Failing to comply with state tax laws can lead to serious financial and legal issues. States impose penalties for late payments, underreporting, and non-filing, often coupled with steep interest rates. These charges vary widely by state, with some applying flat fees and others using percentage-based penalties that escalate over time. For example:

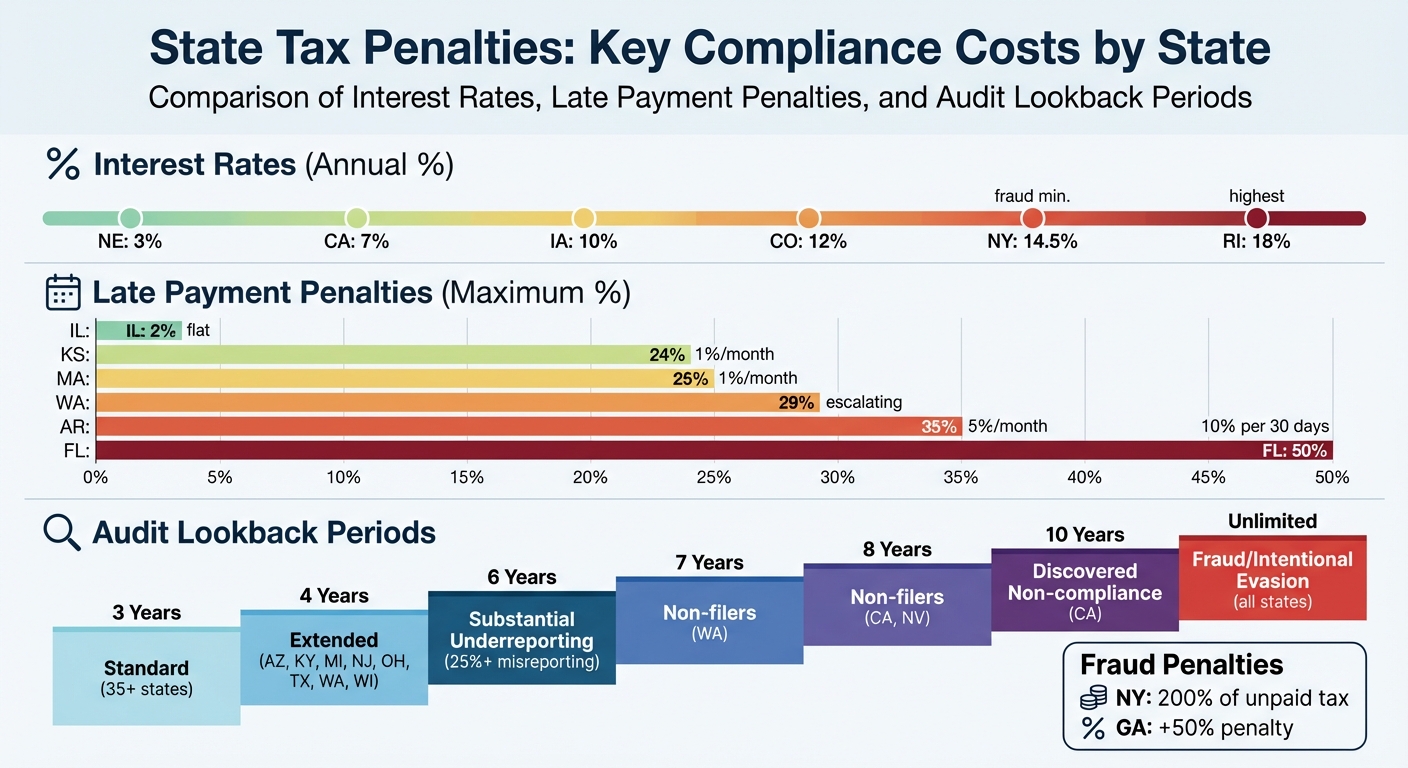

- Interest Rates: Range from 3% (Nebraska) to 18% (Rhode Island).

- Late Payment Penalties: Washington charges up to 29%, while Arkansas caps at 35%.

- Fraud Penalties: New York doubles the unpaid tax, and Georgia adds 50%.

- Audit Lookback Periods: Typically 3 years but can extend to 7–10 years for unfiled or fraudulent returns.

Non-compliance can also lead to suspended permits, asset seizures, and tax liens. For businesses operating in multiple states, understanding these rules is critical to avoid escalating costs. Compliance strategies, like timely filing and keeping detailed records, are essential to mitigate risks.

State Tax Penalties Comparison: Interest Rates, Late Payment Penalties, and Audit Lookback Periods

What Are Sales Tax Penalties For Late Payments?

1. Penalty Rates by State

When it comes to tax penalties, states take different approaches – some base their penalties on percentages, while others impose flat rates. Often, the higher of the two applies. Let’s break down the variations to better understand how states handle late payments and filings.

High-penalty states tend to escalate quickly. For instance, Washington starts with a 9% penalty for payments that are 1–30 days late, bumps it up to 19% for delays of 31–60 days, and tops out at 29% for anything over 60 days late. Florida uses a different approach, adding 10% for every 30 days past due, capping this at 50% of the tax owed. Similarly, Arkansas charges 5% per month, with a maximum penalty of 35%.

On the other hand, low-penalty states take a slower approach. Kansas and Massachusetts, for example, charge 1% per month, with caps set at 24% and 25% respectively. Illinois applies a flat 2% late payment penalty, while penalties for late filing range from 2% to 20%, depending on the circumstances.

Some states also enforce flat-rate minimums, ensuring they collect a fee even if no taxes are owed. Texas, for instance, charges a $50 fee for every late report, regardless of the tax amount due. New York follows a tiered system: a $50 penalty for returns with no tax due, and a minimum of $100 if the return is more than 60 days overdue. Both Georgia and Indiana set their flat-rate minimums at $5.

For fraudulent violations, the penalties are much harsher. New York imposes a civil penalty equal to 200% of the unpaid tax for fraudulent non-payment. Georgia adds an extra 50% penalty for fraud. These charges are in addition to standard late filing and payment penalties, making fraud an extremely costly mistake.

"California penalties apply even if you underreport by small amounts. Always reconcile with local district rates carefully." – Reuben Mattinson, Founder, RJM Tax Exemption

2. Interest Charges by State

Understanding how interest charges accumulate is crucial for grasping the full financial impact of tax non-compliance. While penalties are often imposed upfront, interest charges steadily add to the total amount owed over time, further increasing the overall liability.

Interest rates differ significantly across states. For instance, in 2025, Colorado charges a 12% annual interest rate, which drops to 9% for early payments. Iowa applies a steady 10% rate for both 2025 and 2026. Georgia calculates interest by adding 3% to the Federal Reserve’s prime rate. Meanwhile, California sets its rate at 7% for the second half of 2025, and New York enforces a minimum 14.5% rate in cases involving fraud.

The way interest compounds also affects the total cost. New York uses daily compounding with quarterly rate adjustments. Colorado calculates interest on a daily basis by dividing the annual rate by 365 or 366 days. Iowa accrues interest monthly at a rate of 0.8%, which equals 10% annually. Georgia employs a similar monthly accrual method.

The complexity increases with frequent rate changes and varying rules, especially as states shift toward destination-based sourcing. This makes accurate calculations critical, as even small errors can lead to significant increases in liabilities.

Looking at historical trends, it’s clear how unpredictable interest rates can be. For example, Iowa’s rate peaked at 17% in 1982 before dropping to 5% in 2022. Similarly, Colorado’s discounted rate has fallen to as low as 3% in recent years. These fluctuations underscore the challenge of relying on consistent interest rates over time.

sbb-itb-e2944f4

3. Audit Lookback Periods

Audit lookback periods play a critical role in determining a business’s tax exposure, alongside penalties and interest. These periods define how far back auditors can examine your records, starting from the later of the filing date or due date. Knowing these timeframes is key to understanding your financial risk.

The standard lookback period in most states is three years, which applies to about 35 states and the District of Columbia. However, some states – like Arizona, Kentucky, Michigan, New Jersey, Ohio, Texas, Washington, and Wisconsin – extend their lookback periods to four years. Minnesota, meanwhile, has a unique 3.5-year timeframe. These standard periods can change depending on the accuracy of your filings.

Certain conditions can stretch these periods significantly. For instance, substantial underreporting (misreporting 25% or more of owed taxes) triggers a six-year lookback in states such as Alabama, Arizona, and Florida. In Maine, this threshold rises to 50%, but South Carolina and Vermont set the bar lower at 20%.

"If the auditor believes that the tax base is misrepresented by a certain amount (typically 25%), then the statute of limitations can usually be increased to a much larger time frame." – Alex Oxford, Founder, TaxValet

Failing to file returns or engaging in fraud creates even bigger risks. If no return is filed, the statute of limitations doesn’t begin, leaving businesses open to indefinite liability. For example, Washington imposes a seven-year lookback plus the current year for unregistered taxpayers, while California and Nevada extend this to eight years. Fraud or intentional evasion removes all time limits in nearly every state, allowing auditors to review records dating back to when the business began.

"When a business fails to file required returns, the statute of limitations typically doesn’t begin running. This means the tax authority can assess taxes indefinitely until a return is filed." – Dan Peisner, Sr. Project Manager, The Sales Tax People

Understanding these extended lookback periods is vital to fully grasp the financial consequences of non-compliance.

Pros and Cons

When examining state-specific tax penalty structures, it’s clear that each approach comes with its own set of benefits and challenges. Understanding these trade-offs is crucial for evaluating compliance risks and planning effectively.

Tiered penalty systems provide a level of predictability, enabling businesses to estimate potential costs in advance. However, states that impose monthly accrual penalties, like Georgia’s 5% per month rate, can see those costs climb quickly if issues aren’t resolved in a timely manner. On the other hand, capped penalty structures help limit maximum financial exposure while still encouraging compliance. These systems often reflect the complexity of interest and audit policies, each with its own unique risks.

States with variable rates, such as Georgia’s Federal Reserve prime rate plus 3%, tie penalties to economic conditions. This means rates may drop during economic downturns, potentially reducing costs. In contrast, fixed minimum rates – like New York’s 14.5% for fraudulent failure to pay or Wisconsin’s 18% – remain steady regardless of market fluctuations. While fixed rates provide certainty for financial planning, they can lead to higher costs over time.

The standard 3-year lookback period used by most states offers limited exposure for businesses that maintain compliance. However, states like Texas, Washington, and Ohio extend this window to 4 years, increasing the risk of audits but potentially catching issues earlier. Voluntary Disclosure Agreements, which often cap lookbacks at 3–4 years, provide a structured path to compliance. In contrast, California’s potential 10-year lookback for discovered non-compliance introduces significant uncertainty and risk.

Flat fees offer simplicity but can disproportionately impact smaller transactions. Meanwhile, percentage-based penalties scale with tax liability, making them more equitable but harder to predict. States that include reasonable cause provisions allow penalties to be waived for legitimate errors, but proving reasonable cause can be time-consuming and requires thorough documentation. These nuances underscore the importance of proactive compliance strategies to avoid escalating penalties and unexpected costs.

Conclusion

State tax penalties can vary widely, and the financial impact of non-compliance is no small matter. Interest rates alone range from 9% to a steep 18%, with Rhode Island leading at the highest rate. Penalties in some states can exceed 25%, and the consequences of non-compliance can quickly escalate. For example, in March 2022, a New York window store owner faced over $125,000 in unpaid sales tax, along with an additional $110,000 in interest – nearly doubling the original amount owed.

Audit lookback periods add another layer of risk. While most states stick to a standard 3- to 4-year window, others extend it significantly. Washington, for instance, stretches the period to 7 years for unregistered taxpayers, while California can dig back as far as 10 years in cases of discovered non-compliance. Fraud or unremitted collected sales tax? Those have no statute of limitations in any state.

"Sales tax is a trustee tax. This means that the corporate shield will not protect against sales tax violations."

- Chris Vignone, Managing Director, Indirect Tax, Source Advisors

To mitigate these risks, businesses need strong compliance strategies. Proactive registration can make a big difference. For example, in Washington, voluntarily registering before the state contacts you limits the assessment period to 4 years plus the current year, instead of the full 7 years if discovered. Filing zero returns during periods of no taxable sales is also critical, as skipping filings can trigger penalties. Additionally, Voluntary Disclosure Agreements often cap lookback periods at 3–4 years and may reduce or even waive penalties for disclosed past-due liabilities.

Maintaining electronic records is another essential step, especially for supporting reasonable cause claims if penalties arise. In New York, failing to provide auditable electronic records could result in penalties of up to $5,000 per quarter. For ecommerce businesses navigating complex state regulations, Emplicit offers tailored compliance support across platforms like Amazon, TikTok Shops, Walmart, Target, and direct-to-consumer websites. Their expertise in account health management and custom strategies can help businesses stay ahead.

Since penalties and interest are non-deductible, prevention is far more cost-effective than dealing with the aftermath. Register in every state where you have nexus, meet filing deadlines consistently, and maintain detailed records to shield your business from escalating costs and potential disruptions.

FAQs

What steps can businesses take to avoid state tax penalties?

To steer clear of hefty state tax penalties, businesses need a reliable compliance strategy. The first step? Register for the correct sales tax permits in every state where your business has a nexus – whether it’s physical or economic. Make sure these registrations are always up-to-date. Accurate record-keeping is just as critical. Be meticulous about tracking all transactions and the tax collected. Missing or late filings can lead to penalties ranging from $50 to as much as 30% of the tax owed if delayed for more than 60 days.

Tax laws aren’t static, so staying informed is essential. For instance, economic nexus thresholds, introduced after the South Dakota v. Wayfair decision, have reshaped compliance requirements for many businesses. As your obligations evolve, keeping up with these changes can save you from unexpected issues. If you do spot an error in your filings, filing a voluntary disclosure agreement might help you reduce penalties and interest.

For added peace of mind, consider leveraging ecommerce compliance tools or working with expert partners. These solutions can automate tax calculations, handle filings, and keep track of deadlines. Emplicit is one such partner offering end-to-end services to simplify compliance, minimize errors, and help you avoid penalties – so you can focus on growing your business.

What happens if you don’t file your state tax return?

Failing to file your state tax return can hit both your wallet and your peace of mind. The financial repercussions start with civil penalties – typically a minimum fee of about $50 – and can escalate to 10% of the tax owed per month, maxing out at 30% of the total owed. On top of that, interest keeps piling up on unpaid taxes, making the amount you owe grow steadily over time.

But it doesn’t stop there. States can take serious collection measures, like placing liens on your property, which can complicate your financial life even further. If you continue to ignore your tax obligations, things can take a legal turn. Persistent non-compliance may lead to criminal charges, with penalties ranging from hefty fines to potential jail time. Staying on top of your state tax responsibilities isn’t just smart – it’s essential to avoid these costly and stressful outcomes.

What is an audit lookback period, and how does it impact tax liability?

An audit lookback period sets the timeframe during which a state auditor can review your sales tax filings to check for compliance. For instance, if a state’s lookback period is three years, auditors can only examine returns filed within the three years leading up to the filing date or the due date, depending on which is later. This means any transactions within that window could result in additional taxes, interest, or penalties if discrepancies are found.

However, under certain circumstances, states may extend this period – sometimes to five years or longer – if they suspect fraud, gross negligence, or substantial underreporting (typically 25% or more). For ecommerce sellers, this extended timeframe can significantly increase potential liabilities, as it opens the door to reviewing a larger volume of past transactions.

Partnering with a reliable service like Emplicit can help businesses stay ahead by ensuring accurate tax records, streamlining filings, and minimizing the risk of unexpected penalties.