Selling internationally? It’s a huge opportunity, but cross-border tax compliance can be tricky. Mistakes like misclassifying products or ignoring VAT rules can lead to fines, shipment delays, or even account suspensions on platforms like Amazon. Here’s what you need to know:

- VAT Compliance: VAT rates vary by country, and sellers need to register and remit taxes based on customer location. For low-value EU imports (€150 or less), the IOSS simplifies this process.

- Customs Duties: Duties are calculated based on product classification (HS codes), value, and origin. Starting July 2026, the EU will impose a flat €3 duty on low-value shipments.

- Regional Tax Rules: The U.S., UK, and EU each have unique thresholds and filing requirements. For instance, U.S. sellers must navigate state sales tax rules, while UK sellers face VAT from their first sale.

- Avoiding Hidden Costs: Non-compliance can mean fines averaging $10,000 per incident, abandoned carts (39% due to surprise fees), and frustrated customers.

Key takeaway: Accurate tax calculations and proper registrations are critical for protecting profits and maintaining customer trust. Dive into the details to stay ahead.

Mastering 8 Key Cross-Border Topics: What You Need to Know | Decoding Cross-Border Ecommerce | Ep 49

sbb-itb-e2944f4

Value-Added Tax (VAT) for International Ecommerce

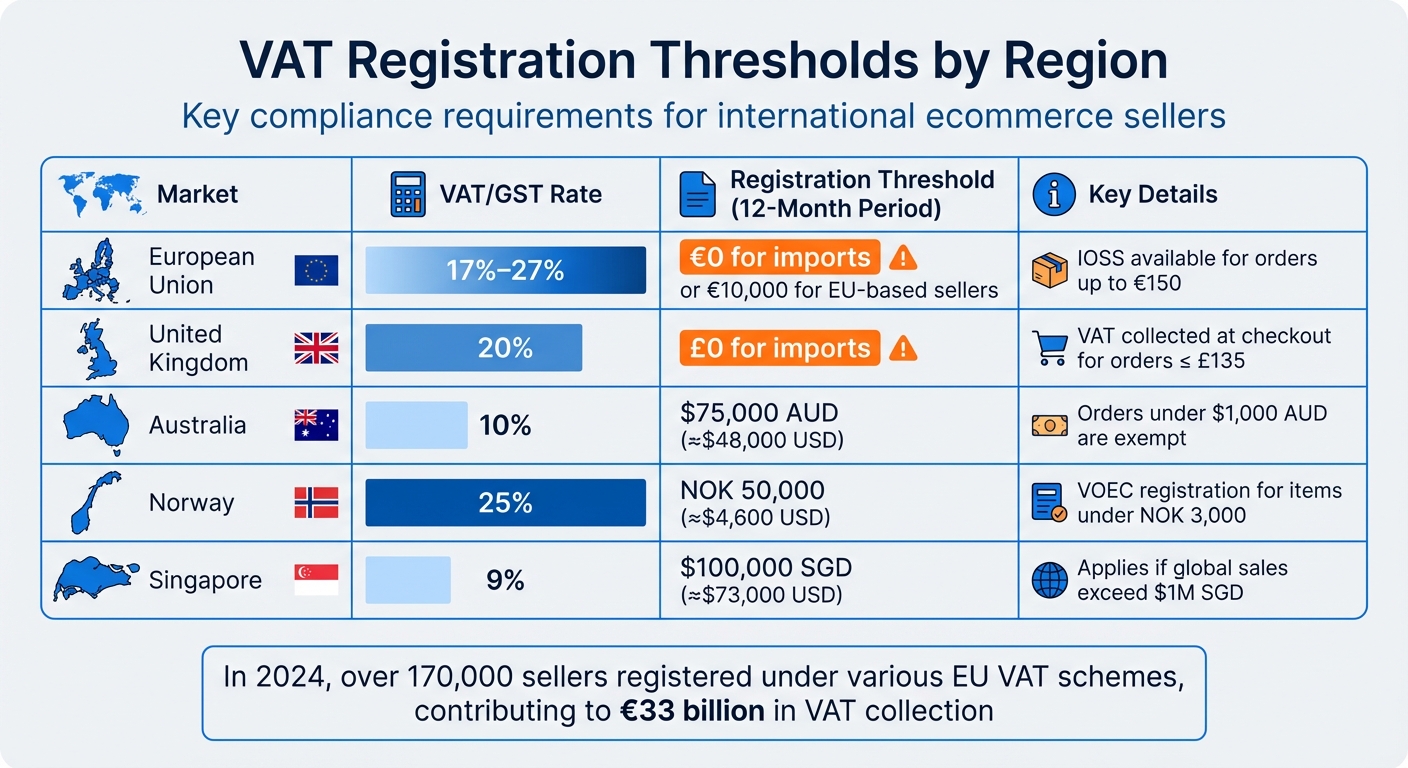

VAT Registration Thresholds and Rates by Country for Ecommerce Sellers

How VAT Applies to Cross-Border Sales

VAT is a consumption tax applied throughout the supply chain, with the final cost passed on to the consumer. It follows a destination-based principle, meaning the tax is due in the country where the customer receives and uses the goods.

As the seller, you’re tasked with collecting VAT at checkout and remitting it to the appropriate tax authorities in the destination country. For business-to-consumer (B2C) transactions, this involves charging the correct VAT rate based on the customer’s location. In business-to-business (B2B) sales, the reverse charge mechanism often applies, shifting the responsibility to the business customer.

Globally, over 170 countries operate under a VAT system. In the EU, rates range from 17% to 27%, with an average of about 21%. Digital services like SaaS and downloads are taxed in more than 80 jurisdictions, often with little to no registration threshold. Additionally, storing inventory in a foreign fulfillment center – such as through Amazon FBA in Europe – typically requires immediate VAT registration in that country, regardless of sales volume.

Next, we’ll look at how registration thresholds determine when VAT obligations come into play.

VAT Registration Thresholds by Region

Registration thresholds dictate when international sellers must register to collect VAT locally. In many cases, these thresholds are minimal or don’t exist at all. For instance, in the EU and UK, non-resident businesses must account for VAT from the very first sale.

| Market | VAT/GST Rate | Registration Threshold (12-Month Period) | Key Details |

|---|---|---|---|

| European Union | 17%–27% | €0 for imports or €10,000 for EU-based sellers | IOSS available for orders up to €150 |

| United Kingdom | 20% | £0 for imports | VAT collected at checkout for orders ≤ £135 |

| Australia | 10% | $75,000 AUD (≈$48,000 USD) | Orders under $1,000 AUD are exempt |

| Norway | 25% | NOK 50,000 (≈$4,600 USD) | VOEC registration for items under NOK 3,000 |

| Singapore | 9% | $100,000 SGD (≈$73,000 USD) | Applies if global sales exceed $1M SGD |

In 2024, over 170,000 sellers registered under various EU VAT schemes, contributing to €33 billion in VAT collection – up from €26 billion in 2023. Since these systems launched, they’ve facilitated nearly €88 billion in VAT collection. Exceeding mid-year thresholds triggers immediate VAT registration.

Import One-Stop Shop (IOSS) for EU VAT Compliance

The Import One-Stop Shop (IOSS) is an online system designed to simplify VAT compliance for business-to-consumer imports into the EU valued at €150 or less. Instead of registering in multiple EU countries, sellers can register once in a single Member State and handle all EU VAT obligations through a single monthly return.

When using IOSS, you collect VAT at the local rate during checkout (e.g., 20% for France or 19% for Germany), then submit a monthly return and payment to your designated Member State. A valid IOSS ID in customs declarations exempts goods from VAT at importation, reducing surprise fees for customers and speeding up delivery.

"For consumers, the upfront collection of VAT through the IOSS prevents unwanted surprises or delays at customs." – LookupTax

Non-EU sellers, including those in the US and UK, must appoint an EU-based intermediary to register for IOSS and manage filing requirements. Sellers are required to keep detailed transaction records for 10 years and file a nil return even during months with no sales. Persistent non-compliance, such as missing three consecutive payments, results in removal from the scheme for two years.

The IOSS took effect on July 1, 2021, coinciding with the EU’s removal of the €22 VAT exemption for low-value imports. This change is estimated to generate over $7.6 billion (€7 billion) in additional annual tax revenue for EU member states. With approximately 12 million low-value parcels entering the EU daily – totaling 4.6 billion parcels in 2024 – the IOSS has become a crucial tool for ensuring smooth customer experiences without border delays.

Proper VAT management not only ensures compliance but also builds trust by eliminating unexpected costs for customers. Up next, we’ll dive into customs duties and how they impact your cross-border tax strategy.

Customs Duties for Ecommerce Sellers

When shipping internationally, ecommerce sellers face customs duties, which are separate from VAT and serve as charges for goods crossing borders. These duties are designed to protect local industries and generate revenue for governments. To price products accurately and safeguard profit margins, understanding how customs duties work is critical.

How Customs Duties Are Calculated

The formula for calculating customs duties is simple: Customs Duty = Customs Value × Tariff Rate. However, accurate calculations depend on three key factors: HS Classification, Valuation, and Country of Origin.

- Harmonized System (HS) Code: This global product classification system uses a standardized format. The first six digits are universal, with additional digits defined by individual countries for their tariff schedules. Using the wrong code can lead to overpayment, penalties, or delays. For complex products, consider requesting a binding tariff information ruling to ensure legal accuracy.

- Valuation: Most countries base duties on the Transaction Value, which reflects the actual price paid for goods. The valuation method varies:

- CIF (Cost, Insurance, Freight): Includes the invoice price plus shipping and insurance to the destination port. This is common in the EU.

- FOB (Free On Board): Covers costs up to the export point and is used in markets like the United States.

The landed cost often includes more than just the base duty. It may factor in VAT or GST on the duty-paid value, excise duties for certain products, customs processing fees, and carrier disbursement fees (typically 2.5% of the duty value or a $15 USD minimum). For example, Section 232 tariffs on steel and aluminum can average 50%.

EU Customs Duty Changes (July 2026)

Starting July 1, 2026, the EU will introduce major changes, including the removal of the €150 customs duty exemption. Instead, a flat €3 duty will apply to low-value ecommerce shipments. This shift addresses the surge in cross-border ecommerce, with 4.6 billion low-value parcels entering the EU in 2024 – a 100% increase from 2023, with 91% originating from China.

Key details of the €3 flat duty:

- Applies per tariff heading, not per parcel. For example:

- A shipment containing three different products (e.g., phone case, screen protector, charging cable) incurs a €9 charge (€3 × 3).

- Ten identical items in one parcel count as one tariff heading and incur only a €3 duty.

"Multi-SKU cross-border shipments could face €6, €9, €12, or even higher duties depending on the makeup of the order." – J&J Global Fulfilment

This flat duty is temporary, lasting until mid-2028, when standard EU customs tariffs based on HS codes will resume. The change is expected to generate €1–2 billion annually for the EU. For context, a €10 item could see a price increase of 30% once the duty is applied.

Adding complexity, some EU member states are introducing national handling fees:

- Romania: €5 per shipment (January 2026)

- France: €2 per item (March 2026)

- Italy: €2 per package (later in 2026)

- EU-wide handling fee: €2 per parcel under consideration.

| Date | Region | Change | Fee Structure |

|---|---|---|---|

| January 1, 2026 | Romania | National Handling Fee | €5 per shipment |

| March 1, 2026 | France | National Handling Fee | €2 per item |

| July 1, 2026 | European Union | Removal of €150 Exemption | €3 flat duty per item |

| November 2026 | European Union | EU-wide Handling Fee | Approx. €2 per parcel |

| Mid-2028 | European Union | Permanent Customs Regime | Standard EU tariff rates |

Adjusting Prices to Include Customs Duties

To handle customs duties effectively, ecommerce sellers can choose one of three strategies: absorb the cost, pass it to customers, or localize inventory.

- Absorbing the Duty: Covering customs fees yourself can simplify the customer experience and help maintain conversion rates. This approach works best for sellers with healthy margins or low EU sales volumes.

- Passing Costs to Customers: Using a Delivered Duty Paid (DDP) model ensures transparency by showing the full landed cost upfront. This reduces cart abandonment and refused deliveries. Tools like landed cost calculators can help capture all fees, including duties, VAT, and handling charges, in real time.

- Localizing Inventory: Storing stock in EU-based warehouses eliminates per-order customs duties. Instead, you pay bulk import tariffs, which are often more economical for high-volume sellers. This also speeds up delivery times and enhances the customer experience.

To minimize the impact of per-item charges, analyze your EU order data from the past year. Look for trends in basket composition and the number of tariff classifications per order. If you sell product bundles, group items under the same HS code to reduce €3 charges per shipment. Ensure accurate HS code assignments for all products to avoid penalties or overpayment.

Tax Requirements by Region

Tax policies differ widely depending on where you operate. The United States, United Kingdom, and European Union each have their own thresholds, filing systems, and compliance requirements. Grasping these differences is critical for setting accurate prices and avoiding fines.

United States Tax Requirements

The U.S. uses a state-level sales tax system with over 13,000 jurisdictions spanning 45 states and the District of Columbia. Five states – Alaska, Delaware, Montana, New Hampshire, and Oregon – do not impose a statewide sales tax.

Economic nexus rules require sellers to collect sales tax if they exceed $100,000 in sales or 200 transactions in a state. Even a minor physical presence, such as storing inventory in a warehouse or attending a trade show, can establish nexus. Sellers must first obtain a state sales tax permit before collecting tax. For foreign sellers, a U.S. Employer Identification Number (EIN) is typically required to register. States like California and Texas have simplified compliance by focusing solely on revenue thresholds – both have a $500,000 threshold with no transaction requirement. New York, however, still requires $500,000 in sales and 100 transactions.

Marketplace facilitator laws place the responsibility of collecting and remitting sales tax on platforms like Amazon, eBay, and Etsy. However, sellers must maintain proper records for 3 to 7 years to prepare for potential audits.

Tax rules around products can vary significantly. For example, clothing is tax-exempt in Pennsylvania but taxable in most other states. Digital goods and SaaS are also treated inconsistently. Combined state and local tax rates can exceed 10% in states like Louisiana (10.11%) and Puerto Rico (11.50%). To manage this complexity, tools like TaxJar (starting at $19/month) or Avalara AvaTax ($50 to $200+/month) can calculate rates based on exact ZIP+4 addresses.

The de minimis exemption for imports, which previously allowed shipments under $800 to enter duty-free, ended on August 29, 2025. Now, most imports are subject to customs duties. Keep in mind, this is separate from sales tax, which applies at the state or local level.

| State | Economic Nexus Threshold | Notable Rule |

|---|---|---|

| California | $500,000 | No transaction threshold |

| New York | $500,000 and 100 transactions | Higher threshold for small sellers |

| Texas | $500,000 | No transaction threshold; SaaS is 80% taxable |

| Florida | $100,000 | No transaction threshold |

| Most States | $100,000 or 200 transactions | Standard "Wayfair" threshold |

United Kingdom Tax Requirements

The UK operates under a VAT system, requiring overseas sellers to register from their very first sale, as there is no threshold for them. In contrast, UK-based businesses only need to register after exceeding £90,000 in taxable turnover.

The £135 rule determines VAT collection methods. For goods valued at £135 or less, VAT is collected at the point of sale. For goods over £135, VAT is usually collected as import VAT at the border. The standard VAT rate is 20% for most goods and digital services.

Overseas sellers must register for VAT immediately if they store inventory in the UK or use fulfillment centers like Amazon FBA. Marketplaces often act as "deemed suppliers" for orders under £135, collecting and remitting VAT directly to HMRC. Sellers are still required to provide a valid UK VAT number to avoid account suspension.

VAT registration for overseas businesses generally takes 4 to 6 weeks, so starting the process at least 30 days before your first sale is advisable. You may need to submit passport copies and official business documents to verify your application. Businesses outside the UK and EU might also be required to appoint a UK VAT representative.

The Making Tax Digital (MTD) initiative, mandatory by 2026, requires all VAT-registered businesses to use HMRC-approved software for record-keeping and filing quarterly returns. Manual submissions are no longer accepted, and records must be stored digitally for at least 6 years.

| Seller Type | Registration Threshold | Key Requirement |

|---|---|---|

| UK-Established Business | £90,000 taxable turnover | Register once the threshold is exceeded |

| Overseas Seller (No UK Base) | £0 (Nil) | Register before the first sale |

| Distance Selling (EU to NI) | £70,000 | Applies to goods moved from the EU to NI |

| Inventory Stored in UK | £0 (Nil) | Immediate registration required |

European Union Tax Requirements

In the EU, VAT applies to all imports, regardless of value, following the abolition of the €22 VAT exemption on July 1, 2021. For intra-EU distance sales, a €10,000 threshold applies. Below this, sellers can charge their home country’s VAT; above it, VAT of the destination country is required.

The IOSS scheme simplifies VAT collection for non-EU sellers on B2C imports valued at €150 or less. However, this requires appointing an EU fiscal representative. For goods above €150, Delivered Duty Paid (DDP) shipping can prevent customers from facing unexpected fees upon delivery.

Storing inventory in an EU warehouse requires immediate VAT registration in that country, regardless of sales volume. Digital services like SaaS are always taxed at the customer’s location.

EU VAT rates must be at least 15%, though they vary by country. In 2022, EU Member States collected over €17 billion through the OSS system, a 26% increase from 2021. However, VAT fraud and non-compliance still cost an estimated €89.3 billion.

Non-compliance with IOSS rules, such as missing three consecutive monthly filings, results in being barred from the scheme for two years. Additionally, alcohol and tobacco products are excluded from both IOSS and OSS schemes.

Starting July 1, 2026, the EU will remove the €150 customs duty exemption, meaning all imports will also incur customs duties. France will also introduce a €2 "Taxe Petit Colis" handling fee for low-value imports cleared under simplified procedures, effective March 1, 2026.

| Scheme | Coverage | Key Requirement |

|---|---|---|

| IOSS | B2C imports ≤ €150 from non-EU to EU | VAT collected at checkout; monthly return |

| OSS | Intra-EU B2C distance sales & services | Quarterly return; single registration |

Setting Up Tax Compliance Systems

Establishing a strong tax compliance system involves registering for necessary programs, assigning responsible parties, and keeping detailed, audit-ready records.

How to Register for IOSS

The Import One-Stop Shop (IOSS) simplifies VAT compliance for business-to-consumer (B2C) sales of low-value goods (up to €150) imported into the EU. This excludes excise goods like alcohol and tobacco. To register, use the Member State of Identification (MSI) portal and provide your business details, tax numbers, and website. Once registered, you’ll receive a 12-digit IOSS VAT ID starting with "IM." If working with an intermediary, ensure you complete the online declaration form within 28 days of starting the process.

"The Import One Stop Shop (IOSS) has been created to simplify the declaration and payment of VAT for distance sales of low value goods not exceeding 150€ imported from third territories or third countries." – European Commission

Your IOSS number must be included on every customs declaration to benefit from "green channel" clearance, which prevents VAT charges at the border. Monthly returns are mandatory – even if no sales occur – and failing to file for three consecutive periods may result in a two-year suspension from the program. Using IOSS can drastically reduce VAT-related administrative tasks, but you must retain transaction records for 10 years from the end of the year the supply was made.

Once registered with IOSS, the next step is designating an Importer of Record (IoR) to handle customs compliance.

Appointing an Importer of Record (IoR)

The Importer of Record (IoR) is responsible for ensuring imported goods meet local regulations, including filing necessary paperwork and covering duties and taxes. In the U.S., acting as an IoR requires either a U.S.-based business entity with an EIN or a U.S. resident with an SSN. Foreign entities must register as non-resident importers and fulfill bonding requirements. Many businesses rely on licensed customs brokers to act as their IoR, granting them authority through a Power of Attorney (POA). For frequent imports, a continuous bond is recommended, as it covers all shipments for the year. Keep in mind that most commercial imports valued over $2,500 require a customs bond.

The IoR is directly accountable for all customs duties and taxes. Under the UK IOSS program, both you and your intermediary share liability for VAT debts. Additionally, U.S. customs law mandates keeping import records for at least 5 years from the date of entry.

After setting up IOSS and appointing an IoR, the next critical step is maintaining precise records to support compliance efforts.

Tax Documentation and Record-Keeping

For EU VAT schemes, businesses must retain detailed records of transactions for at least 10 years. These records should include product descriptions, quantities, values, customer details, invoices, VAT rates, payment evidence, and proof of returns. Record gross revenue first, then deduct platform fees, refunds, and discounts as separate items. Using only net deposits, such as Amazon payouts, can lead to understated revenue and incorrect tax calculations. Additionally, ensure that landed costs like freight, duties, insurance, and handling are factored into your cost of goods sold (COGS) for accurate margin reporting.

When dealing with cross-border sales in non-Euro currencies, VAT returns should use the European Central Bank (ECB) exchange rate from the last day of the reporting period. To streamline compliance, integrate your tax settings across e-commerce platforms, ERP systems, and accounting software. Tools like TaxJar, Avalara, or Vertex can automate tax rate calculations and filings across multiple regions.

| Business Volume | Reconciliation Frequency | Rationale |

|---|---|---|

| Under 100 orders/month | Monthly | Low volume allows for batch processing |

| 100–1,000 orders/month | Bi-weekly | Reduces the risk of discrepancies |

| 1,000–10,000 orders/month | Weekly | High volume requires frequent checks |

| Over 10,000 orders/month | Daily (Automated) | Manual processes become impractical |

Keep all tax-related documents, such as completed forms, government communications, and certificates, in a centralized folder for easy access during audits or registrations. Regularly review your sales volumes against regional thresholds to identify new registration needs and avoid penalties.

Conclusion

To manage cross-border tax compliance effectively, start by auditing your VAT and GST registrations in every market where you operate. Double-check that your product HS codes are accurate to avoid shipment delays that could cost both time and money. Non-compliance fines average around $10,000 per incident, and 63% of small and medium-sized businesses in cross-border trade encounter unexpected costs due to compliance errors.

Integrating tax calculation software with your checkout system is a smart move. This ensures customers see the full landed costs upfront, reducing manual errors and preventing 39% of cart abandonments caused by surprise fees. For EU sales under €150, registering for IOSS can save up to 30% in administrative time while speeding up customs clearance. Keep all invoices, shipping proofs, and customs declarations securely stored in PDF/A or XML formats for 7–10 years. Additionally, maintaining a compliance calendar helps you track filing deadlines and avoid penalties – missing deadlines in countries like Spain can lead to fines as high as 300% of unpaid taxes. Strong record-keeping is essential for adapting to ever-changing compliance requirements.

Regular compliance audits and monitoring sales volumes against country-specific thresholds are key to staying on top of your obligations. As your business grows, consider working with a customs broker – costs typically range from $1,000 to $5,000 per month – or adopting a Merchant of Record model to shift compliance responsibilities to a third party.

With the global ecommerce market projected to hit $8.09 trillion by 2027, businesses that master cross-border tax compliance are well-positioned to tap into this growth. Review your registrations, confirm your HS codes, and automate tax calculations at checkout to stay competitive.

FAQs

When do I need to register for VAT abroad?

If your sales surpass the local VAT threshold – such as €10,000 in the EU – or if you store inventory in warehouses located in another country, you are required to register for VAT in that region. These situations establish tax obligations, meaning you’ll need to adhere to the specific VAT regulations of the country involved.

Do I need IOSS or DDP for EU orders?

For EU orders, the IOSS (Import One Stop Shop) scheme can help streamline VAT compliance for low-value shipments, making the process simpler. Alternatively, using DDP (Delivered Duty Paid) allows you to handle customs duties and VAT at checkout, which can increase customer confidence and improve their shopping experience. The best option depends on your business model and the nature of your orders.

How can I avoid HS code duty mistakes?

To prevent errors with HS codes, it’s crucial to classify products with precision. Use detailed product information, such as the material, purpose, and how the product is constructed. Avoid making assumptions or recycling codes from similar items without proper verification, as these mistakes can result in delays or increased duties.

Instead, take the time to verify HS codes based on the specific details of your product or consult relevant customs resources for guidance. By ensuring accurate classification, you can reduce the risk of errors, stay compliant with regulations, and avoid customs delays or surprise fees.