Selling on marketplaces in 2026 comes with complex tax challenges. Here’s what you need to know:

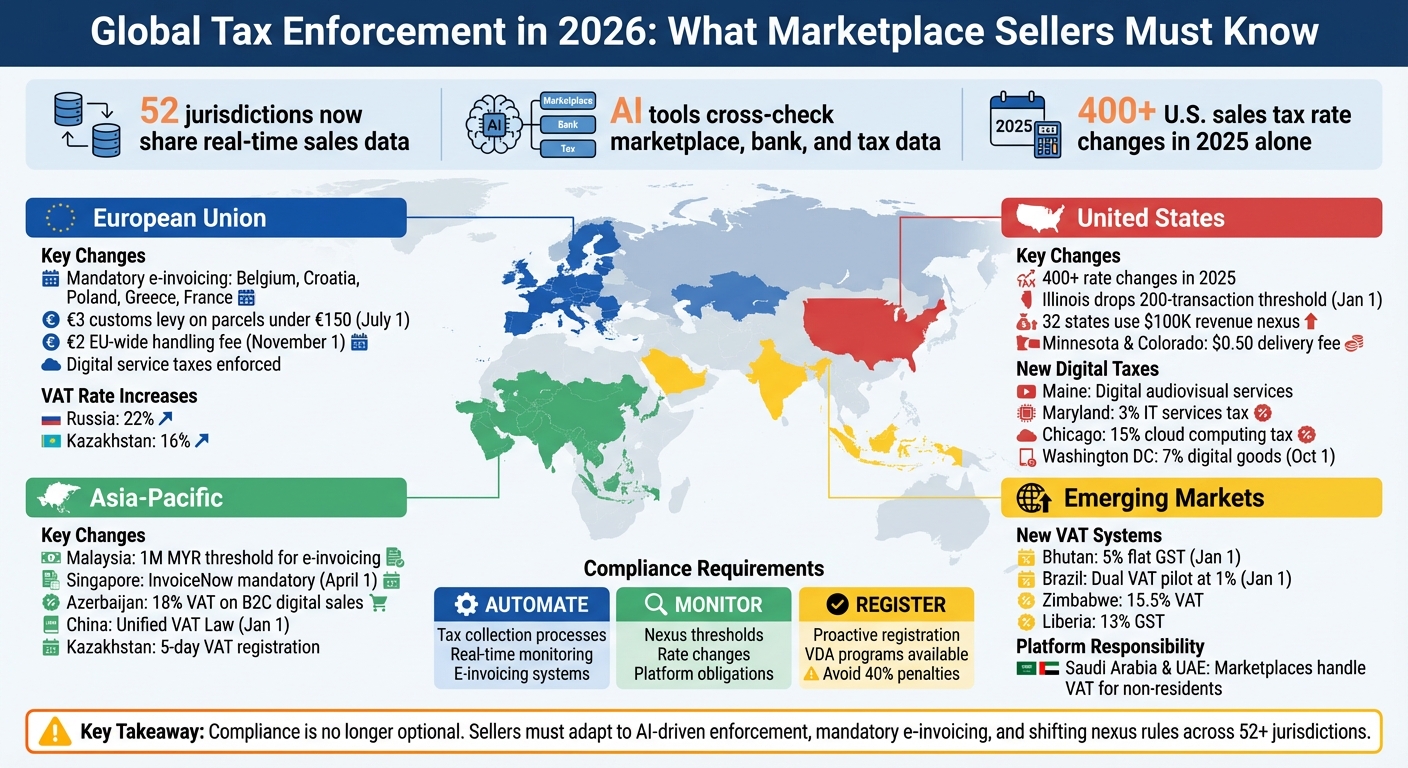

- Global Tax Enforcement is Tightening: Authorities in 52 jurisdictions now share real-time sales data, making compliance harder to evade. AI tools are widely used to cross-check marketplace, bank, and tax data.

- Major VAT/GST Updates:

- The EU introduced mandatory e-invoicing in countries like Belgium, Poland, and France.

- VAT rates are increasing in key markets (e.g., Russia: 22%, Kazakhstan: 16%).

- Starting July 1, the EU will eliminate customs relief for low-value imports, replacing it with a €3 levy on parcels under €150.

- U.S. Tax Changes:

- States are expanding sales tax categories and lowering nexus thresholds, with over 400 rate changes in 2025 alone.

- Local district taxes are becoming more intricate, with overlapping rates and new fees like Minnesota’s $0.50 delivery charge.

- Emerging Markets Join the Game:

- Bhutan and Brazil introduced new VAT systems.

- Countries like Saudi Arabia and UAE now require marketplaces to handle VAT for non-resident sellers.

- Digital Service Taxes: The EU and other regions are enforcing taxes on digital goods and services, increasing seller costs.

Key Takeaway: Compliance is no longer optional. Sellers must automate tax processes, monitor changing rules, and account for new costs like VAT, customs duties, and digital service taxes. Ignoring these changes risks audits, penalties, and lost profits.

2026 Global Tax Changes for Marketplace Sellers by Region

Unlocking Your 2026 Strategy: TikTok Pay On Behalf, US EPR, and VAT Disruptions

sbb-itb-e2944f4

Major VAT and GST Changes in 2026

Big shifts in tax regulations across the EU, Asia-Pacific, and emerging markets are changing the way marketplace sellers handle compliance. These updates are shaping the strategies sellers need to adopt to stay on track.

EU Mandatory E-Invoicing Requirements

In 2026, several EU countries rolled out mandatory e-invoicing for VAT-registered businesses. Here’s a quick look at the changes:

- Belgium: From January 1, domestic B2B transactions must use the Peppol network.

- Croatia: Also from January 1, B2B and B2G transactions require compliance with the Fiscalization 2.0 system.

- Poland: Large taxpayers (annual revenue over PLN 200 million) must comply with the KSeF platform starting February 1, with all VAT-registered businesses following by April 1.

- Greece: B2B e-invoicing is required for businesses with annual revenue exceeding €1 million starting February 2, expanding to all businesses by October 1.

- France: From September 1, all businesses must be able to receive e-invoices, while large and mid-sized companies must also issue them.

These mandates mean sellers must generate invoices in structured, machine-readable formats like XML, UBL, or CII. To comply, businesses need to upgrade their ERP or accounting software, connect to government systems or certified Peppol Access Points, and validate country-specific identifiers (e.g., France’s SIREN/SIRET or Poland’s NIP) to avoid rejected invoices. For marketplace sellers, adapting to these digital invoicing requirements is now a must.

Asia-Pacific GST for Digital Goods

Asia-Pacific countries are tightening GST rules for digital goods and services:

- Malaysia: Starting January 1, businesses with annual sales over 1 million MYR must issue invoices through a government platform.

- Singapore: All new voluntary GST registrants must use the InvoiceNow system from April 1. Financial support of 1,000 to 5,000 SGD is available to help with the transition.

- Azerbaijan: Non-resident digital service providers are required to register and apply an 18% VAT on B2C sales from January.

- Pakistan: Online marketplaces and payment intermediaries must withhold and deposit sales tax on goods ordered digitally.

- Kazakhstan: The mandatory VAT registration period is now just five business days after turnover exceeds 40 million tenge (around $88,000), with electronic invoice validation becoming the norm.

- China: The new unified VAT Law, effective January 1, introduces specific rules for digital platform intermediaries.

These updates highlight the growing complexity of tax compliance in the region.

VAT/GST Adoption in Emerging Markets

Emerging markets are also stepping up their tax game:

- Bhutan: A national GST at a flat 5% replaces the sales tax system starting January 1.

- Brazil: A pilot dual VAT system kicks off the same day with a 1% combined "test" rate.

Several countries are tweaking tax rates and thresholds:

- Zimbabwe: Increased its VAT rate from 15% to 15.5% on January 1.

- Liberia: Raised its GST from 12% to 13%.

- South Africa: Upped its VAT registration threshold from ZAR 1 million to ZAR 2.3 million per year as of February 2026, giving smaller sellers more breathing room.

A noticeable trend is the shift in VAT collection responsibility to marketplace platforms. For example:

- Saudi Arabia and UAE: Online marketplaces are now responsible for VAT on digital services sold by non-resident vendors to local customers.

- Kazakhstan: Non-resident sellers must obtain a Business Identification Number (BIN) through a notarized confirmation letter and translated proof of incorporation.

Emerging markets are no longer easy tax havens. They’re evolving into complex regulatory environments, much like established economies. Sellers must stay vigilant, monitor platform-level VAT obligations, and ensure proper documentation for cross-border transactions.

US Tax Changes: Sales Tax and Digital Taxation

In 2026, U.S. states are introducing new tax rules that will impact marketplace sellers significantly. These changes include expanding taxable categories, tightening oversight, and lowering nexus thresholds. Sellers must adapt quickly to ensure compliance.

State Sales Tax Expansion

States are targeting the digital economy to increase tax revenue. Starting January 1, 2026, Maine will tax digital audiovisual and audio services like Netflix and Spotify. Maryland has introduced a 3% tax on IT services, web hosting, and application publishing. Georgia now taxes specific digital products, such as e-books and digital art sold with permanent usage rights. Washington state has extended its tax to include B2B services like advertising and website development, while Washington, D.C. will raise its sales tax on digital goods and services from 6% to 7% on October 1, 2026. Meanwhile, Chicago has increased its cloud computing tax to 15% for 2026.

These changes mean sellers offering digital products, SaaS, or IT services may now face tax obligations in areas where they previously didn’t. Complicating matters further, states often define digital products differently, leading to potential confusion. Local tax variations are expected to add another layer of complexity.

Local District Taxes and Rate Changes

Local tax rates are becoming more intricate. A single ZIP code can now include multiple overlapping tax rates due to special district taxes that fund local projects. In some states, combined state and local tax rates can exceed 11%.

For sellers in "Home Rule" states like Colorado, Alabama, and Louisiana, compliance is even more challenging. These states allow local jurisdictions to operate independently as taxing authorities, meaning sellers may need separate business licenses and must file multiple tax returns. Louisiana, with its 64 parishes, is particularly complex for accurate tax mapping.

Additionally, Minnesota and Colorado have introduced a $0.50 Retail Delivery Fee on qualifying orders. Minnesota applies this fee to deliveries over $100.

"A single ZIP code can now contain multiple, overlapping tax rates, creating an enormous compliance headache and making manual sales tax management nearly impossible." – TaxJar

As these tax rates evolve, nexus rules are also undergoing significant changes.

Lower Nexus Thresholds

Many states are simplifying nexus rules by removing transaction-count thresholds. Starting January 1, 2026, Illinois joined Alaska, Utah, and North Carolina in eliminating the 200-transaction requirement, opting instead for a revenue-only model. Currently, over 32 states use a $100,000 annual revenue benchmark for economic nexus, while 18 states still include transaction thresholds.

This shift benefits sellers with many low-value transactions but increases risk for those selling high-ticket items, as they may cross the revenue threshold with fewer sales. Some states, like Illinois, include gross sales in their calculations, while others count only taxable sales. Marketplace sales from platforms such as Amazon, Walmart, and Etsy are typically included in these calculations.

| Nexus Category | Threshold Metric | Key States |

|---|---|---|

| Revenue Only | $100,000 | IL, AZ, CO, FL, UT, WA, WY |

| High Revenue Only | $500,000 | CA, TX |

| Dual Requirement (AND) | $500k AND 100 Transactions | NY |

| Revenue OR Transactions | $100k OR 200 Transactions | GA, LA, MD, NJ, OH |

States are increasingly using AI tools to enforce compliance. New York, California, and Michigan now cross-check marketplace data from platforms like Amazon and Etsy against tax filings to identify non-compliant sellers. Penalties for non-compliance are steep – up to 40% of the tax owed if caught during an audit. Maryland imposes an interest rate of 11.48% on delinquent taxes.

For sellers with past exposure, Illinois offers the Remote Retailer Amnesty Program from August 1 to October 31, 2026, which allows liabilities to be settled without interest. Washington state’s Voluntary Disclosure Agreement program, running February 1 to May 31, 2026, can waive up to 39% of penalties and limit the look-back period to 3–4 years.

Global Tax Policies Affecting eCommerce

Starting January 1, 2026, tax authorities worldwide are stepping up enforcement efforts using advanced data analytics. This marks a new phase of "enforcement maturity", reshaping strategies for marketplace sellers across the globe. In regions like the EU, Middle East, and Asia, authorities are now cross-referencing VAT and GST filings with platform transaction data in real time.

These tightening regulations on digital service taxes and customs duties are significantly influencing costs for sellers, whether they deal in physical goods or digital services. To safeguard margins, sellers need a clear understanding of these interconnected policies.

Digital Service Taxes in the EU and Other Regions

Digital service taxes are hitting marketplace sellers hard this year. For instance, in March 2026, Amazon announced it would increase its Digital Services Fee (DSF) from 2% to 3% of referral and FBA fees in the UK, France, Italy, and Spain. This change, effective March 20, 2026, shifts the burden of national digital service taxes directly to sellers based on their sales location.

To put this into perspective, a seller generating $1M in sales with $270k in referral and FBA fees would see an additional $2,700 in costs from the 1% DSF hike. This can quickly eat into margins. Sellers are encouraged to establish recovery processes for unreimbursed losses and fee discrepancies, which often amount to 1% to 3% of total revenue. Additionally, calculating margins on a country-by-country basis, instead of treating the EU as a single market, can help sellers better navigate these changes.

Beyond Europe, other regions are also introducing new taxes. Manitoba (Canada) and Mauritius, for example, have implemented taxes targeting non-resident digital service providers. Meanwhile, countries like Saudi Arabia, UAE, and India, as well as the EU, have moved from developing policies to actively enforcing them for cross-border digital services. This shift is increasing audit risks for marketplace sellers.

Tariff Changes on Marketplace Goods

Customs duties are also undergoing significant revisions, further complicating the compliance landscape for cross-border sellers. In the EU, the €150 customs duty exemption for small parcels will be eliminated on July 1, 2026. Instead, a fixed customs duty of €3 will apply to all EU-imported parcels valued under €150. Additionally, an EU-wide customs handling fee of €2 per line is set to take effect in November 2026.

Individual EU member states are layering additional fees on top of these EU-wide charges. For example, Romania has introduced a national logistics fee of approximately €5 (RON 25) for sub-€150 shipments as of January 1, 2026, while Italy has implemented a €2 customs handling fee for similar shipments starting the same date. These overlapping fees require sellers to adjust their cost management strategies immediately.

"The reforms aim to, amongst others, create a level playing field between e-commerce and traditional retail, cover increasing costs of customs supervision and improve VAT collection." – Bird & Bird

In the U.S., new tariffs are also making waves. Following a Supreme Court ruling on IEEPA, a 10% global tariff was introduced under Section 122 on February 24, 2026, with plans to potentially raise it to 15%. Additionally, the U.S. and Switzerland have agreed on a reciprocal 15% cap on customs duties, replacing previous rates as high as 39%. Meanwhile, Thailand has essentially eliminated its de minimis threshold by lowering it from 1,500 baht to just 1 baht, effective January 1, 2026.

To navigate these changes, sellers might consider adding a transparent "Tariff Adjustment Fee" at checkout to maintain profitability while keeping customers informed. Exploring options like shifting production to regions with lower tariff exposure or sourcing materials domestically could also help. Updating pricing models and ERP systems to reflect these layered fees and rising landed costs will be crucial.

Compliance Strategies for Marketplace Sellers

Marketplace sellers face mounting challenges as VAT, GST, and local tax regulations continue to evolve. Tax authorities are now using AI to cross-check marketplace data with payment records, making manual processes outdated. States like New York, California, and Michigan are already leveraging these advanced tools, leaving automation as the only viable option for staying compliant.

Managing sales tax manually across 46 states can take up to 69 hours each month. Unsurprisingly, 86% of businesses now outsource at least one tax function to handle the growing complexity. Missing even one threshold can lead to automatic audits, emphasizing the need for thorough compliance strategies. It’s clear that sellers must rethink their approach to compliance.

Automation and Real-Time Tax Monitoring

Integrated tax systems are now essential for marketplace sellers. These systems need to consolidate sales data from multiple channels while distinguishing between marketplace sales – where platforms act as the "deemed supplier" – and direct-to-consumer sales. This prevents errors like double taxation or missed filings. Sellers also need tools that can handle the complexities of overlapping jurisdictions, from city taxes to special taxing districts.

For sellers operating in the EU, adopting government-approved e-invoicing systems is mandatory. Countries like Greece, Belgium, Croatia, Poland, and Slovenia are gradually rolling out these systems through 2026.

"E-invoicing is no longer a passing trend, it’s a fundamental shift in how global businesses manage compliance. Companies can no longer afford a patchwork of local solutions for each mandate."

- Matt Hammond, General Manager of E-Invoicing at Avalara

Real-time reporting is increasingly replacing quarterly filings as tax authorities use transaction data to identify discrepancies. Monthly reconciliations of marketplace reports, direct sales, and payment processor data are critical to catching issues before they trigger audits.

Nexus Monitoring for Multistate Sellers

Automation alone isn’t enough – sellers also need to actively monitor nexus requirements. Economic nexus thresholds are changing rapidly. For instance, as of January 1, 2026, Illinois, Alaska, and Utah will drop their "200 transactions" trigger, relying solely on a $100,000 revenue threshold. While this simplifies compliance for high-volume sellers, it could surprise low-volume sellers dealing with high-ticket items. In just the first half of 2025, U.S. states implemented over 400 sales tax rate changes, a 25% increase compared to 2024.

Nexus isn’t just about sales anymore. Physical presence, whether through third-party logistics (3PL) warehouses, remote employees, or affiliate marketing, can create tax obligations. Sellers using services like Amazon FBA should routinely check where their inventory is stored, as moving stock across state lines can introduce new compliance requirements.

Real-time alerts from tax software can notify sellers when they’re nearing revenue thresholds, allowing them to register before tax collection becomes mandatory. Registration must occur before taxes are collected, as operating without a permit can lead to penalties even if taxes are later remitted. If past obligations were overlooked, voluntary disclosure agreements (VDAs) can reduce the lookback period to 3–4 years and waive up to 39% of potential penalties. For example, Maryland’s 11.48% interest rate on delinquent taxes highlights the importance of early disclosure.

Upgrading Tax Engines for Scalability

As digital tax enforcement ramps up globally, scalable tax solutions are becoming indispensable. Modern tax engines must integrate seamlessly with omnichannel platforms and retain at least four years of transaction data to meet audit requirements.

Automating exemption certificate management is another must-have feature. Errors in collecting or renewing resale certificates can lead to significant liabilities during audits. Digital tools that track certificates and send renewal reminders can help avoid these pitfalls.

AI and machine learning are no longer optional. Advanced tax engines use these technologies to analyze data, reconcile transactions, and forecast future liabilities based on growth trends. They can also flag potential compliance risks before they escalate into audits, a critical feature as tax authorities adopt similar technologies.

For global sellers, tax engines must support structured e-invoicing to comply with the EU’s VAT in the Digital Age (ViDA) initiative. The "Reinvent with Tax" market, which focuses on digital tax transformation, is expected to grow at a 12.55% CAGR through 2033, highlighting the importance of scalable solutions.

The ideal approach combines high-speed automation for routine tasks with human expertise for complex, multi-state compliance challenges.

"Technology doesn’t eliminate your responsibility to understand what’s happening. You’re still the captain of this ship and the software is just a really helpful first mate."

- Arvin Faustino of CapForge

Conclusion

Global tax enforcement has embraced AI-driven, real-time data sharing across 52 jurisdictions, enabling authorities to cross-check VAT returns with platform and bank records seamlessly. The European Union’s introduction of a €3 customs levy on parcels under €150 – along with an extra €2 handling fee starting November 1, 2026 – signals heightened scrutiny on even the smallest transactions.

These regulatory shifts are already impacting marketplace sellers. In at least seven countries, including Belgium, Croatia, Poland, Greece, and the UAE, B2B e-invoicing is now mandatory, effectively phasing out manual processes. Additionally, platforms like Amazon and eBay are now required to handle VAT collection in 29 countries, putting the onus on sellers to close any compliance gaps.

Preparation is no longer optional. Sellers who conduct thorough gap analyses, automate tax collection processes, and keep a close eye on nexus thresholds can avoid costly penalties tied to reactive compliance. Pricing strategies also need to evolve – factoring in upfront duties and taxes rather than waiting until delivery. By building these costs into their pricing models, sellers can safeguard their profit margins and maintain customer trust as enforcement becomes increasingly rigorous.

Proactive registration offers a safer path forward. As Dr. Lena Vogt from the OECD Centre for Tax Policy and Administration notes:

"A ‘wait-and-see’ approach is now statistically riskier than proactive registration – even for micro-sellers".

Ultimately, combining proactive registration, automation, and real-time monitoring will be crucial for sellers to navigate the tightening global tax landscape effectively.

FAQs

Do I need to register for VAT/GST if the marketplace collects it for me?

If the marketplace handles VAT or GST collection for you, you generally won’t need to register for these taxes on your own. That said, you’re still accountable for following local tax regulations, which might include submitting additional filings to tax authorities. Make sure you’re clear on your responsibilities to steer clear of any complications.

What should I change before EU e-invoicing becomes mandatory for my sales?

To stay compliant with the latest EU regulations, make sure your systems are aligned with updated standards like EN 16931-1. This standard ensures your e-invoicing processes meet the necessary requirements for cross-border transactions.

The EU’s 2030 digital VAT strategy is also introducing real-time transaction reporting. This means businesses will need to adapt their digital reporting processes to handle these new demands. Take the time to review and upgrade your invoicing and reporting tools now, so you’re prepared for these changes.

How can I track sales tax nexus across multiple U.S. states without missing thresholds?

To keep tabs on sales tax nexus across different U.S. states, consider using tools that track your sales against state-specific thresholds. Most states set their limit at $100,000 in annual sales. However, states like California and Texas often have higher thresholds, such as $500,000, or might rely on transaction-based criteria. Leveraging automated tools and conducting regular reviews of each state’s rules can help you stay compliant and notify you when you approach or exceed those limits.