Selling through a 3PL? Here’s what you need to know about taxes.

If your inventory is stored in a third-party logistics (3PL) warehouse, you may owe taxes in multiple states – even if you’ve never set foot there. This is due to physical nexus, which creates tax obligations based on where your inventory is located. Add in economic nexus thresholds (like $100,000 in sales in many states), and tax compliance becomes a complex challenge.

Here’s a quick breakdown of what matters most:

- Physical Nexus: Storing inventory in a state triggers tax obligations immediately, even if you make no sales there.

- Economic Nexus: States require tax collection once sales exceed thresholds, often $100,000 annually.

- Marketplace Facilitator Rules: Platforms like Amazon handle sales tax for marketplace sales, but direct sales (e.g., Shopify) are your responsibility.

- Penalties for Non-Compliance: States are cracking down, with penalties reaching 10% of unpaid taxes plus interest.

To stay compliant, analyze where your inventory is stored, track sales data, register in nexus states, and automate tax filings. Tools like TaxJar or Avalara can simplify this process. Proper planning and accurate records are your best defense against audits.

What online sellers NEED to know about sales tax nexus

sbb-itb-e2944f4

Understanding Sales Tax Nexus

State-by-State Economic Nexus Thresholds for Multi-State Sellers

The term "nexus", which originates from the Latin word for "a binding together", refers to the legal connection that requires businesses to register, collect, and remit sales tax in a specific state. For businesses using third-party logistics (3PL) providers, nexus can be established in two main ways: through physical presence or economic activity.

Physical Nexus from 3PL Warehouses

Physical nexus is created when a business has a tangible presence in a state. This includes owning offices, employing staff, or storing inventory in a warehouse. Even if the warehouse is owned by a 3PL provider, having inventory stored there qualifies as a physical presence. Unlike economic nexus, physical nexus does not depend on meeting any minimum thresholds. As Eightx explains:

"Physical nexus has no minimum threshold. Even trace amounts of inventory create nexus – you don’t need to make a single sale in that state".

The "dollar one rule" applies here, meaning nexus is established as soon as your first unit of inventory arrives in the state. This rule is particularly significant for Amazon FBA sellers, many of whom unknowingly create nexus in 20 or more states due to Amazon’s practice of redistributing inventory across its fulfillment centers.

Economic Nexus and State Thresholds

Economic nexus is determined by the volume of sales or transactions in a state, regardless of any physical presence. This concept gained traction following the 2018 South Dakota v. Wayfair Supreme Court decision, which allowed states to require sales tax collection from remote sellers based solely on economic activity. Currently, 45 states and the District of Columbia enforce economic nexus laws.

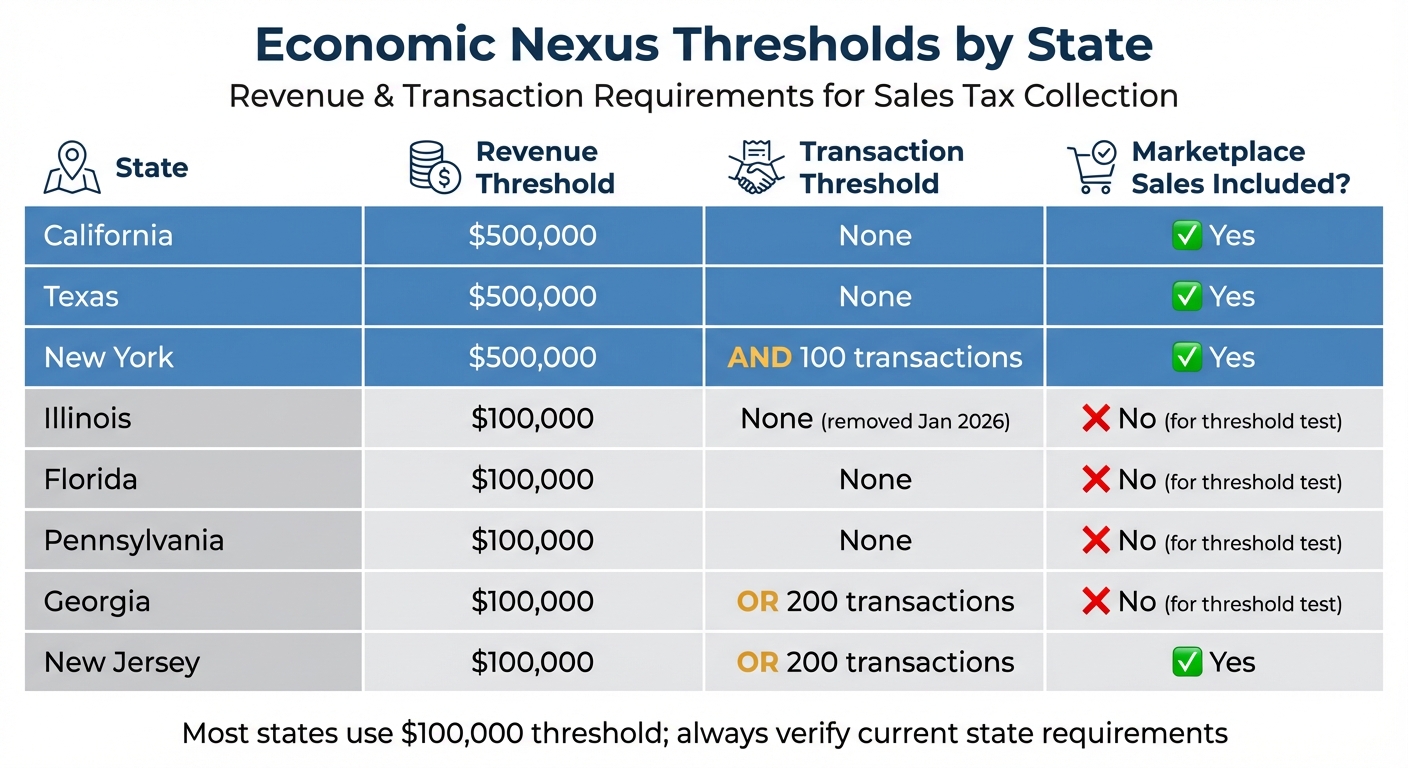

Most states set their thresholds at $100,000 in annual sales or 200 transactions. However, some states, like California and Texas, require $500,000 in sales before economic nexus applies. New York’s threshold is even stricter, requiring both $500,000 in sales and 100 transactions.

Sales made through marketplaces like Amazon count toward your economic nexus thresholds, even if the platform handles tax remittance. If you sell on both a marketplace and your own site (e.g., through Shopify), you must combine sales data from all channels to determine your nexus obligations. Matt Putra from Eightx highlights how these thresholds are calculated:

"Nexus is typically rolling four quarters usually, or rolling quarters, or some combination thereof. It’s like if your last three quarters were at this, now you have nexus, now you have to file".

| State | Revenue Threshold | Transaction Threshold | Marketplace Sales Included? |

|---|---|---|---|

| California | $500,000 | None | Yes |

| Texas | $500,000 | None | Yes |

| New York | $500,000 | AND 100 transactions | Yes |

| Illinois | $100,000 | None (removed Jan 2026) | No (for threshold test) |

| Florida | $100,000 | None | No (for threshold test) |

| Pennsylvania | $100,000 | None | No (for threshold test) |

| Georgia | $100,000 | OR 200 transactions | No (for threshold test) |

| New Jersey | $100,000 | OR 200 transactions | Yes |

Marketplace Facilitator Rules

Marketplace facilitator laws have reshaped how sales tax is handled for sellers using platforms like Amazon, Walmart, Etsy, and eBay. These platforms, rather than the individual sellers, are now tasked with calculating, collecting, and remitting sales tax for transactions processed through their systems. This shift applies in all 45 states with state-level sales tax, as well as in Washington D.C. and Puerto Rico.

A platform qualifies as a marketplace facilitator if it lists products, processes transactions through its checkout system, and collects payments from buyers. One key feature of these laws is the "liability shield", which protects sellers if the platform miscalculates taxes. As SmartSMS explains:

"Marketplace facilitator laws generally include a ‘liability shield’ for sellers. This means if the marketplace calculates or collects the wrong amount of tax, the marketplace – not you – is liable for the error".

However, sellers are still responsible for providing accurate product taxability codes. If a seller categorizes a product incorrectly, they may be held liable for any resulting errors. This distinction helps clarify responsibilities, especially for sellers with inventory stored in multiple states, where tax obligations can quickly become complicated.

Marketplace vs. Direct Sales Tax Obligations

When selling through a marketplace, the platform takes care of tax calculation, collection, and remittance. For direct sales on your own website – using platforms like Shopify or WooCommerce – you are entirely responsible for ensuring compliance. Marketplace sales also contribute to your economic nexus thresholds. For example, if your total sales across Amazon and your website exceed $100,000 in a state, you may trigger economic nexus, requiring you to collect tax on your direct sales. However, states like Texas and Washington exclude marketplace-facilitated sales from these calculations.

In some states, even when a marketplace collects all applicable taxes, you might still need to register and file informational "zero-dollar" returns if you establish nexus through third-party logistics (3PL) inventory storage. To ensure accurate filings and avoid double-counting revenue, it’s important to pull monthly marketplace tax reports – like Amazon’s "Marketplace Tax Collection Report" – and reconcile them with your direct sales data. Understanding these distinctions is essential for staying compliant with multi-state tax requirements.

Tax Compliance Roadmap

Once you’ve grasped the concepts of sales tax nexus and marketplace facilitator rules, the next step is to create a structured tax compliance plan. This involves understanding your obligations in each state, registering where necessary, automating processes, and maintaining compliance over time.

Conduct Nexus Analysis

The first step is pinpointing where you’re required to collect sales tax. For 3PL sellers, physical nexus is established as soon as your inventory is stored in a third-party warehouse – even if you didn’t select that location. To identify where this applies, review your Amazon Inventory Event Detail report for the past 12–24 months. Many FBA sellers discover they have nexus in over 20 states at once due to Amazon’s automated inventory distribution system.

Next, assess economic nexus by analyzing your sales data by ship-to state and sales channel. Most states set a $100,000 annual sales threshold, but some – like California, Texas, and New York – have a higher limit of $500,000. Pay attention to how states measure this threshold: some use the "Prior Calendar Year", while others rely on a "Rolling 12-Month Period." Even if your sales later fall below the threshold, you might still need to collect sales tax for 1–4 calendar quarters, depending on state rules.

Once you’ve mapped out your nexus obligations, the next step is to ensure your products are taxed correctly.

Review Product Taxability

Tax rules vary widely by state, and not all products are taxed the same way. For instance, clothing might be tax-exempt in certain states, while digital goods, SaaS products, and food items are subject to differing tax rates and rules. Carefully review your product catalog and assign the correct tax codes based on each state’s definitions to avoid errors in tax collection.

After verifying product classifications, take steps to simplify and automate your tax processes.

Automate Tax Processes

Manually calculating taxes for multiple states is not only time-consuming but also prone to mistakes. Tax automation software can handle this complexity by integrating with your ecommerce platform – whether it’s Shopify, Amazon, or an ERP system. These tools calculate the correct tax rate at checkout based on the customer’s location and can also manage exemption certificates and audit documentation. Features like AutoFile can even prepare and submit tax returns automatically, helping you meet deadlines.

For businesses selling through multiple channels, automation can also reconcile taxes collected by marketplaces with those from direct-to-consumer sales, avoiding double-counting issues. Popular tools like TaxJar, Avalara, and Vertex are widely used for these purposes. To stay on top of expanding obligations, consider hiring a fractional CFO or CPA to oversee your tax automation and ensure new nexus states are added as your 3PL network grows.

Register and Set Up Filing Systems

Once you’ve identified your nexus states, register for a sales tax permit. This should be done within 30–60 days of exceeding economic thresholds or immediately upon establishing physical nexus. You’ll need your Federal EIN, business name, NAICS code, owner SSNs, and the date nexus was established. After registering, set up a filing calendar based on your tax liability.

If your business operates in multiple states, the Streamlined Sales Tax (SST) registration system can simplify the process by allowing you to apply for permits in 24 participating states with a single application. While most state permits are free, processing can take 2–4 weeks. Always secure your permit before collecting tax to avoid penalties for unremitted taxes.

Even if you have no taxable sales during a period, you’re still required to file returns. Set up a system to store exemption certificates and establish monthly reconciliation procedures. In states like Colorado and Louisiana, which have home-rule jurisdictions, you may need to register and file separately with local authorities, in addition to state-level returns.

Contract Review and Audit Preparedness

Your 3PL contract isn’t just a business agreement – it’s a legal document that outlines tax responsibilities. Typically, these contracts state that the seller is fully responsible for determining where sales tax needs to be collected. Katherine Gauntt, Senior Manager at BDO USA, LLP, explains: "The 3PF and 3PL contracts will specify that the seller is solely responsible for determining where sales tax should be collected and what products and fees are subject to sales tax". Even though your 3PL manages billing, the legal responsibility for charging and remitting accurate sales tax remains yours. This clarity in roles is essential for audit preparedness.

Key 3PL Contract Clauses to Review

While automating tax processes and establishing nexus are important, your contract with the 3PL also plays a critical role in staying compliant. One key requirement is ensuring that the contract mandates clear reporting of inventory movement. Your 3PL should provide detailed information about where inventory is stored, as redistribution between warehouses could create physical nexus in states you may not have anticipated. Additionally, the contract should require precise "ship-from" and "ship-to" location reports for every order. These details are crucial during audits to demonstrate that the correct tax rates were applied.

Another essential clause involves clarifying whether you’re selling to the 3PL (as a wholesale transaction) or through them (as part of a fulfillment arrangement). This distinction impacts not only sales tax collection but also income tax protections under Public Law 86-272.

For those using Amazon FBA or similar services, ensure your contract includes access to reporting tools that identify inventory locations by state. Amazon sellers, for example, should regularly run "Inventory Event Detail" or "Inventory Ledger" reports to map fulfillment center codes to states where nexus has been triggered.

Documentation for Audit Readiness

Strong contracts are just one piece of the puzzle – thorough documentation is equally important for audit defense. States like California, Pennsylvania, and Washington actively pursue companies with inventory in 3PL warehouses for back taxes. If you’ve triggered nexus but never registered, the audit lookback period can stretch indefinitely, as it’s not limited by the statute of limitations. Penalties for noncompliance can reach 10% of the taxes owed, with interest compounding monthly.

To prepare, maintain monthly reconciliations that separate marketplace-collected taxes (from platforms like Amazon or Walmart) from direct sales (via Shopify, WooCommerce, etc.). This ensures that total gross sales are reported accurately. Archive essential records such as marketplace tax reports, direct sales data, reconciliation spreadsheets, and payment confirmations. For B2B sales, keep valid exemption certificates on file for the specific state of delivery. This type of documentation creates a strong audit trail, demonstrating your compliance efforts and helping to address state inquiries. Together, these contract provisions and meticulous records form a critical part of your overall tax compliance strategy.

Conclusion

Multi-state 3PL sellers face two key triggers for tax obligations: physical nexus from inventory storage and economic nexus once state thresholds are exceeded. Unlike economic nexus, which depends on meeting sales thresholds, storing inventory in a 3PL warehouse creates an immediate tax obligation, regardless of sales volume. As Bennett Thrasher explains:

"Using a 3PL warehouse can create a physical presence in the state where goods are stored. This ‘physical presence nexus’ establishes a direct tax obligation, even when the business has no employees or offices in that state".

To avoid unexpected liabilities, a timely nexus analysis is critical. Start by reviewing your fulfillment reports to identify where inventory is stored and cross-checking sales data against state thresholds. If you find past exposure, consider a Voluntary Disclosure Agreement (VDA) to mitigate penalties. For instance, in March 2025, Wealthovation Global helped an e-commerce client resolve $140,000 in sales tax exposure across 17 states, reducing penalties by 70% through VDAs.

Once nexus states are identified, register for sales tax permits. For participating states, the Streamlined Sales Tax system can simplify the process. If your business operates in multiple states (typically more than 3–5), automation tools like TaxJar, Avalara, or Vertex can streamline real-time tax calculations and filings. After registration, ensure compliance with additional responsibilities under marketplace facilitator rules.

Keep in mind, marketplace facilitator rules don’t eliminate all your obligations. Even if platforms collect sales tax, you’re still required to register in nexus states, file returns (even for $0), and collect tax on direct sales through platforms like Shopify. Additionally, physical presence via 3PL inventory can override income tax protections under Public Law 86-272, potentially exposing your business to state income taxes as well as sales taxes.

Finally, meticulous record-keeping is essential for audit readiness. Maintain detailed documentation of inventory locations, state-specific sales, and exemption certificates. States often target businesses with 3PL inventory during audits, and accurate records will help protect your business. By focusing on proper planning, registration, automation, and record management, you can build a solid framework for multi-state tax compliance.

FAQs

How do I find every state where my 3PL inventory created nexus?

Storing your inventory with a third-party logistics (3PL) provider often establishes a physical nexus in the state where the inventory is housed. This means you’ll likely need to register for sales tax and file returns in that state. On top of that, many states have economic nexus laws. These laws mean that even if you don’t have a physical presence, reaching a certain sales threshold in a state can trigger tax obligations.

To stay on top of these requirements, it’s critical to review each state’s nexus rules and thresholds. You might also want to consult a tax professional or leverage a nexus risk tool to make sure you’re meeting compliance requirements in every state where you do business.

If a marketplace collects tax, do I still need to register or file in that state?

If a marketplace handles tax collection on your behalf, you usually don’t need to register or file taxes in that state – unless your sales exceed nexus thresholds or the state has specific rules that require action. It’s crucial to keep track of your economic activity to stay aligned with local tax regulations.

What should I do if I should have been collecting sales tax in past years?

If you didn’t collect sales tax in previous years, it’s important to take action right away. Start by reviewing where you had a physical or economic nexus – this includes locations where you stored inventory, such as in third-party logistics (3PL) warehouses. From there, file any overdue returns, report your taxable sales, and pay the taxes, penalties, and interest you owe. It’s a good idea to consult a tax advisor to better understand your obligations and develop a plan to stay compliant moving forward. Acting quickly can help minimize penalties and lower the risk of an audit.