If you’re selling on platforms like Amazon, eBay, or Etsy, understanding tax deductions can save you significant money. Deductions reduce your taxable income, meaning you pay taxes only on your profits – not your total revenue. For example, if you’re in the 25% tax bracket, missing a $1,000 deduction could cost you $250 in extra taxes. Here’s what you need to know:

- Key Deductions: Costs like inventory, shipping, platform fees, and advertising are fully deductible.

- Business Structure Matters: Sole proprietors, LLCs, and S-corps have different rules for reporting income and deductions.

- Recordkeeping Is Essential: Keep detailed documentation for every expense to back up your claims.

- Sales Tax Isn’t Deductible: But sales tax on business purchases can be written off.

The right deductions can boost your cash flow, allowing you to reinvest in your business. Up next, we’ll break down specific expenses and how to claim them properly.

Everything Resellers Need to Know About Taxes and Bookkeeping

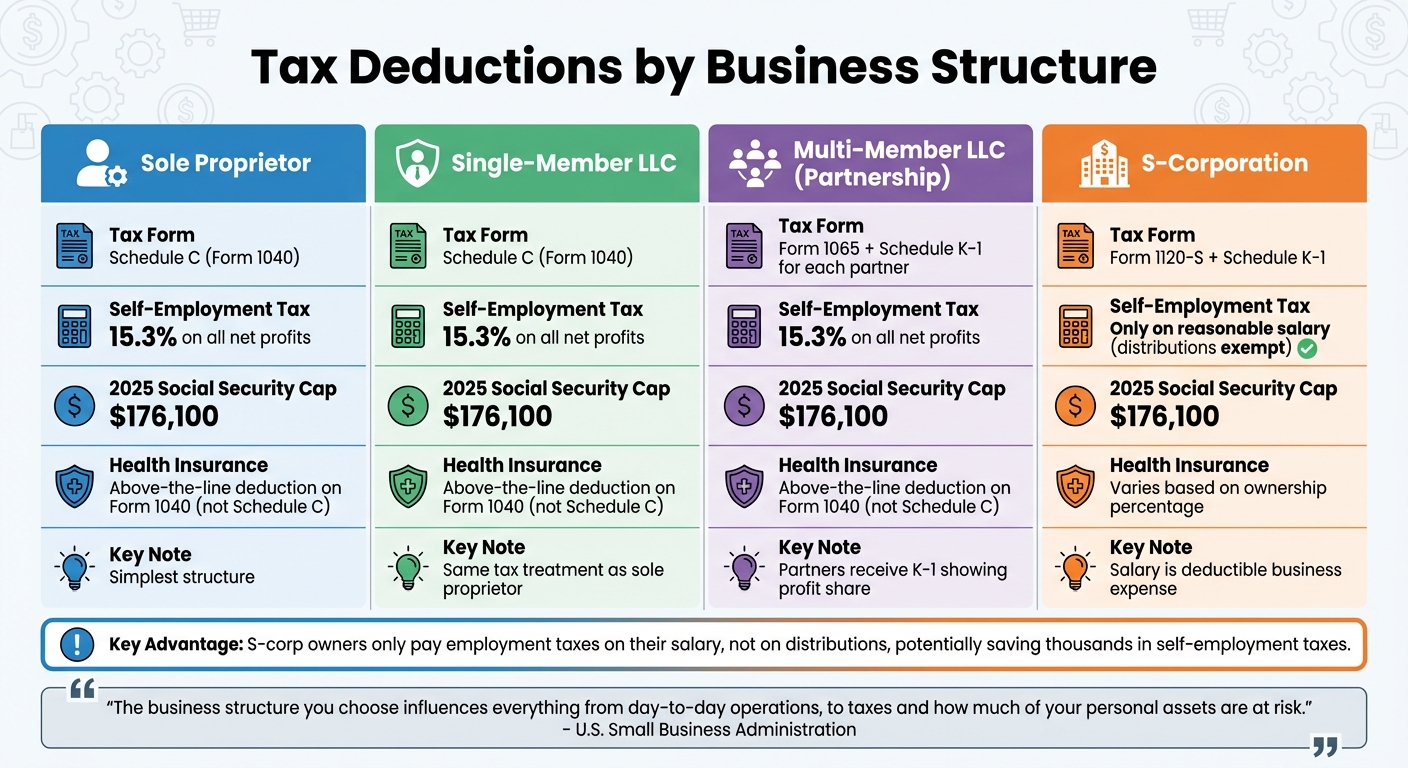

How Business Structure Affects Your Tax Deductions

Tax Deduction Comparison by Business Structure for Marketplace Sellers

The structure of your business directly impacts how you report income and deductions on your tax forms. For example, sole proprietors and single-member LLCs handle their business income and deductions through Schedule C (Form 1040).

On the other hand, multi-member LLCs are treated as partnerships. They must file Form 1065 and issue each partner a Schedule K-1, detailing their share of the profits and deductions. Meanwhile, S-corporations use Form 1120-S and require owners who actively work in the business to pay themselves a "reasonable salary." This salary is considered a deductible business expense.

One major distinction between these structures lies in how self-employment taxes are handled. Sole proprietors and partners pay a 15.3% self-employment tax on all net profits. However, S-corp owners only pay employment taxes on their reasonable salary, while distributions are generally not subject to these taxes. For 2025, the maximum net self-employment earnings subject to the Social Security portion of this tax is capped at $176,100.

Certain deductions, like health insurance premiums, also vary depending on the structure. Sole proprietors and partners, for instance, can claim these premiums as an above-the-line deduction on Form 1040, but not on Schedule C, provided the business is profitable.

"The business structure you choose influences everything from day-to-day operations, to taxes and how much of your personal assets are at risk." – U.S. Small Business Administration

To ensure you’re filing correctly, review your business filings. For example, Articles of Organization confirm an LLC, Form 2553 indicates S-corp election, and married, unincorporated partners might qualify as a Qualified Joint Venture, requiring two Schedule Cs. Knowing your business structure now ensures you can claim the right deductions when it’s time to file.

Tax-Deductible Expenses for Marketplace Sellers

Knowing which expenses you can write off is key to lowering your taxable income. These deductions fall into several categories, each with its own rules. Major deductions – like Cost of Goods Sold (COGS), platform fees, and shipping expenses – are incurred throughout the year. Keeping accurate records ensures you don’t miss out on any eligible write-offs. Let’s dive into the main categories of deductible expenses.

Home Office Deduction

If you use a specific area in your home exclusively and regularly for business, you may qualify for a home office deduction. This space must serve as your principal place of business or be where you meet customers. The IRS also allows deductions for areas used for administrative or management tasks if no other fixed business location is available.

For sellers working entirely from home, even spaces like a basement or garage used to store inventory can qualify. While these areas don’t have to meet the "exclusive use" rule, they must be clearly defined and used consistently for business.

You can calculate this deduction in two ways:

- Simplified method: Deduct $5 per square foot for up to 300 square feet (maximum deduction of $1,500).

- Regular method: Deduct the percentage of your home used for business. This includes a portion of expenses like mortgage interest, rent, utilities, insurance, and repairs. Direct expenses, such as painting your office, are fully deductible, while indirect expenses are prorated based on the business-use percentage.

Inventory and Cost of Goods Sold (COGS)

For most sellers, COGS is the largest deduction. This category includes the purchase price of inventory, freight-in charges, raw materials, and direct labor costs tied to production. However, unsold inventory must remain on your books as an asset until sold – it cannot be deducted immediately.

"The best way to categorize Amazon fees is to list them as COGS and consider them part of the cost of selling your product." – Seller Accountant

COGS also includes related costs, such as packaging materials, shipping fees to move inventory to fulfillment centers, and labor directly involved in production. Tracking these costs carefully ensures you claim the full expense of bringing your products to market.

Shipping and Packaging Costs

All costs tied to delivering products to customers are deductible. This includes postage (USPS, UPS, FedEx), delivery charges, and freight costs for shipping inventory to fulfillment centers like Amazon FBA. Supplies like boxes, poly mailers, bubble wrap, packing peanuts, tape, labels, and printer ink are also eligible.

You can also deduct equipment used for shipping preparation, such as thermal label printers, scales, box cutters, and tape dispensers. For higher-cost equipment, like thermal printers priced over $2,500, depreciation rules may apply, requiring you to deduct the expense over several years instead of all at once.

Don’t forget to track business-related mileage, such as trips to the post office or supply stores. In 2024, the standard mileage deduction rate is $0.67 per mile.

Advertising and Marketing Fees

Promoting your products is another area where deductions can add up. Marketing expenses are fully deductible and cover costs such as:

- Amazon PPC campaigns

- Social media ads on platforms like Facebook, Instagram, and TikTok

- Google Ads

- SEO services

- Payments to influencers for product partnerships

Whether you spend $100 or $10,000 on advertising, every dollar reduces your taxable income. Make sure to maintain detailed records of all advertising costs to maximize your deductions.

Platform Fees and Transaction Costs

Marketplaces and payment processors charge fees that are fully deductible. For example:

- Referral fees from platforms like Amazon, eBay, Etsy, and Walmart

- Monthly subscription fees, like Amazon’s $39.99 Pro Seller plan

- Fulfillment by Amazon (FBA) fees for pick, pack, and shipping services

- Storage fees for inventory in fulfillment warehouses

- Payment processing fees from services like Stripe, PayPal, Square, or Braintree

One challenge with platform fees is that they’re often deducted from your payout before you receive payment. To avoid missing deductions, track gross sales and record fees separately. Many sellers use tools like A2X or Link My Books to sync marketplace data with accounting software like QuickBooks or Xero, ensuring accurate fee tracking and reporting.

Sales Tax and Deductions

When it comes to managing taxes, understanding how sales tax fits into the picture is just as important as tracking your direct business expenses. Sales tax operates differently because you’re essentially a middleman for the state. The money you collect from customers as sales tax isn’t part of your income, and handing it over to the state doesn’t count as a deductible business expense. You’re simply collecting and passing along these funds to the government.

For many online sellers, marketplace facilitator laws simplify the process. Platforms like Amazon, eBay, and Etsy handle the collection and remittance of sales tax on your behalf in most states. However, there are exceptions – New Hampshire, Oregon, Montana, Alaska, and Delaware (known as the "NOMAD" states) don’t require sales tax collection. As eBay puts it: "Once eBay starts to collect tax in the required states, no action is required, and there will be no charges or fees for eBay automatically calculating, collecting, and remitting sales tax". Despite this, some states still require you to register for a sales tax permit and file "zero returns" to report your gross sales – even if the platform is taking care of the tax collection.

While the sales tax you collect from customers isn’t deductible, the sales tax you pay on business-related purchases can be. This tax becomes part of the total cost of an item and is deductible either through COGS (Cost of Goods Sold) or as a supply expense. To avoid paying sales tax upfront on inventory purchases, consider obtaining a resale certificate in states where you have nexus. This certificate allows you to buy inventory tax-free from wholesalers, which not only saves money upfront but also streamlines your deduction strategy.

On your personal tax return, you have the option to deduct either state and local income taxes or state and local sales taxes. These SALT (State and Local Tax) deductions are capped at $40,000 ($20,000 if married filing separately) for tax years 2025–2028. According to Certified Public Accountant Reid Riker, high-income earners often find that the state income tax deduction provides greater savings compared to the sales tax deduction.

Another key aspect to monitor is economic nexus, which can be triggered if you reach 200 transactions or $100,000 in sales in a particular state. If you sell across multiple platforms – such as marketplaces and your own website – you need to track your total sales to determine if you’re required to register for sales tax in specific states. Keep detailed records of all your transactions, including dates, taxes collected, and shipping destinations, for at least three to seven years. This documentation is crucial in case of an audit.

Up next, we’ll dive into how to properly document these transactions for accurate tax filing.

sbb-itb-e2944f4

Documentation and Recordkeeping Requirements

The IRS requires you to back up every deduction on your tax return with detailed records for each transaction.

To stay compliant, set up a structured recordkeeping system. This system should cover four main types of records: gross receipts, resale purchases, business expenses, and assets. For each transaction, make sure to note details like the payee, amount, date, and proof of business use. Whether you prefer software, spreadsheets, or even paper files, the key is to use a system that clearly tracks your income and expenses. Keeping thorough records not only helps you claim deductions but also protects you if you’re ever audited.

Hold onto your records for at least three years from the date you file your return. If you’ve underreported income by more than 25%, keep them for six years. Employment tax records, on the other hand, should be retained for four years. To stay on top of things, record transactions daily and organize your documents by year and expense category. While these practices form the foundation of good recordkeeping, modern tools can make the process even easier.

Today’s accounting software can save you time and effort. Platforms like A2X or Link My Books automatically import marketplace data into systems like QuickBooks or Xero. Receipt management apps can digitize and sort your receipts, while mileage tracking apps such as MileIQ simplify tracking at $0.67 per mile for 2024. For added clarity, use a dedicated business checking account to keep your records accurate and easy to review.

How to Claim Deductions on Your Tax Return

If you’re a sole proprietor or run a single-member LLC, you’ll report your business income and deductions on Schedule C (Form 1040). This form helps determine whether your business ended the year with a profit or a loss. Here’s how to handle it step by step.

Start by selecting your accounting method – either cash or accrual – in Part I. Then, report your total gross receipts before deducting any fees. It’s essential to list your full gross sales instead of just net deposits. Deduct fees separately in Part II to avoid overpaying taxes on income you never received. This approach ensures your entries align with your actual transactions.

In Part II, you’ll itemize operating expenses like advertising, insurance, and supplies. For expenses that don’t fit into standard categories, such as specialized software or unique costs, use Part V. If your business involves selling inventory, complete Part III to calculate your Cost of Goods Sold (COGS). This includes beginning inventory, purchases throughout the year, and ending inventory. For home office deductions, you can either use the simplified method or fill out Form 8829. If you’ve purchased equipment costing over $2,500, report it on Form 4562 for depreciation or Section 179 expensing. Section 179 allows you to expense up to $2.5 million in qualifying purchases for 2025.

If your net earnings reach $400 or more, you’ll need to file Schedule SE to calculate your self-employment tax, which covers Social Security and Medicare at a combined rate of 15.3%. For 2025, the maximum earnings subject to the Social Security portion is $176,100. Additionally, self-employed health insurance premiums can be claimed as an above-the-line deduction on Schedule 1 of Form 1040, not on Schedule C.

To ensure everything is accurate, reconcile your detailed records before submitting your return. Match your entries with documentation such as Form 1099-K to avoid errors. Keep your personal and business finances completely separate – mixing them not only complicates tracking deductions but also raises red flags for audits. If you’re unsure about anything, consulting a tax professional is always a smart move.

Conclusion

To make the most of tax deductions, focus on identifying eligible expenses and keeping thorough records. The largest savings often come from categories like cost of goods sold, platform and transaction fees, shipping costs, advertising expenses, and home office deductions. Every deduction you claim reduces your taxable income, which lowers your overall tax liability.

Remember, the responsibility to prove your deductions rests entirely on you. The IRS requires proper documentation – think invoices, receipts, settlement reports, mileage logs, and even photos of your home office space – to back up your claims. Keeping your business and personal finances separate can make audits less stressful and help avoid potential red flags. Digital tools like QuickBooks or automated receipt storage services can make recordkeeping much easier, aligning with the earlier advice to maintain clear and organized records.

Efficient recordkeeping not only simplifies tax season but also supports your business operations. Running an ecommerce business while staying tax-compliant can feel overwhelming when you’re managing inventory, advertising, and customer service all at once. That’s where Emplicit steps in. They offer a full suite of ecommerce services like marketplace management, PPC optimization, inventory tracking, and account health management. Whether you’re selling on Amazon, Walmart, TikTok Shops, or Target, their USA-based team takes care of the operational complexities. This allows you to focus on scaling your business while staying organized and prepared for tax season.

FAQs

What tax deductions can marketplace sellers claim?

Marketplace sellers have several opportunities to lower their taxable income through common tax deductions. For instance, if you work from home, you might be able to deduct home office expenses, which could include a portion of your rent or utility bills. Similarly, costs related to shipping and packaging, like boxes, tape, and postage, can also be written off.

You can also deduct marketplace fees charged by selling platforms, along with advertising and marketing expenses used to promote your products. Another significant deduction is the cost of goods sold (COGS), which includes the materials and labor involved in creating your products. To make the most of these deductions and stay compliant with IRS rules, it’s crucial to keep thorough records and receipts for all these expenses.

How does my business structure affect the tax deductions I can take?

The business structure you select – whether it’s a sole proprietorship, partnership, LLC, S-corp, or C-corp – plays a key role in determining the tax deductions you’re eligible to claim. For instance, sole proprietors can write off self-employment taxes, health insurance premiums, and retirement contributions using Schedule C. On the flip side, S-corps and C-corps can deduct expenses like employee benefits and other costs incurred at the corporate level. Additionally, some structures, such as S-corps, may qualify for the qualified business income (QBI) deduction, which can further lower taxable income.

The structure you choose can have a significant effect on your tax savings. Understanding how these rules apply to your circumstances is crucial. If you’re uncertain about the best approach, consulting a tax professional can help ensure you take full advantage of the deductions available to your business.

What documents should I keep to claim tax deductions as a marketplace seller?

To claim tax deductions effectively, you need to keep your records well-organized. These records should clearly detail the amount, date, and business purpose of each expense. Some key documents to hang onto include:

- Receipts and invoices for any purchases

- Bank statements and credit card statements

- Canceled checks

- Mileage logs or travel-related records

- Contracts and bills of lading

- Inventory records and expense logs

Staying on top of these documents not only simplifies tax filing but also ensures you’re ready if the IRS ever audits your returns. As a rule of thumb, keep these records for the timeframe recommended by the IRS – usually three to seven years, depending on the type of expense and your specific filing situation.